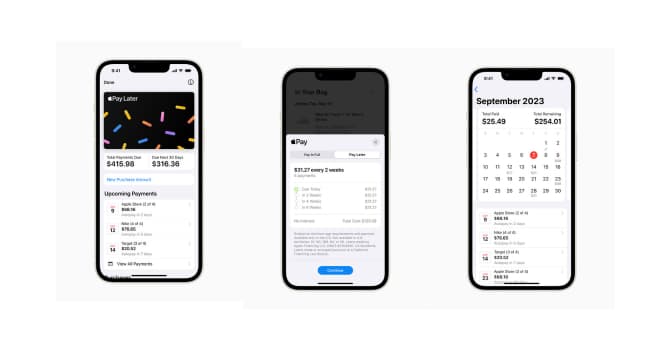

Apple made itself into more of a fintech player this week by announcing the rollout of Apply Pay Later. This is a buy now pay later offering that will be embedded into Apple Wallet

The thing about this launch is that it isn’t really a launch. it is more of a formal introduction. Here is what Apple said in its announcement this week.

“Apple will begin inviting select users to access a prerelease version of Apple Pay Later, with plans to offer it to all eligible users in the coming months.”

So there will not be a wide rollout for a few months. At least.

This steady-as-she-goes rollout might make sense for Apple. It may want to experience the stream of transactions before scaling it up to all Apple Wallet users.

The way the company is approaching this is to invite its test users to apply for Apple Pay Later loans from $50 to $1000, “which can be used for online and in-app purchases made on iPhone and iPad with merchants that accept Apple Pay.”

What’s In It for Apple?

While this announcement has been telegraphed for well over a year, we have to ask ourselves, ‘Why this, why now?’

As my colleague, Mike Boland pointed out to me as we discussed this story today as we recorded next week’s “This Week in Local“ podcast, almost everything Apple does can be tied to one thing. Selling more iPhones.

After all, Apple Pay Later will be baked into Apple Wallet. This adds another iPhone use case that certainly cannot hurt iPhone sales growth.

Yet Mike also notes that iPhone sales are at such a scale that Apple needs revenue diversification to grow. Fintech may be one such path. And how better to increase Apple Wallet use than to add more ways to use it?

“The iPhone, which is its cash cow continues to face revenue deceleration every quarter because of just global saturation of smartphones,” Mike said on the podcast recording, which will air on Monday.

Still, this move just looks a little different than it did when Apple first announced it would step into the BNPL race. BNPL, while enormously popular, is also pretty toxic, given its growing reputation for fueling overspending by consumers, particularly younger consumers. So much so that many BNPL players have started to resist using the term “buy now, pay later” to describe themselves.

Reputational Risk

Does Apple really want to tie its reputation up in this?

Its announcement this week included a few hints that Apple is aware of this challenge. For example, Apple is going with a zero-interest approach.

“Apple Pay Later was designed with our users’ financial health in mind. So it has no fees and no interest and can be used and managed within Wallet, making it easier for consumers to make informed and responsible borrowing decisions,” said Jennifer Bailey, Apple’s vice president of Apple Pay and Apple Wallet, in the announcement.

Even if it doesn’t charge interest and late fees, common ways BNPLs make money, Apple could benefit from greater use of Apple Pay. Or again, from helping to generate additional iPhone sales. Still, we do wonder if BNPL as an industry continues down its current rocky path if Apple might regret its decision to launch Apple Pay Later.